The Opportunity

Manufactured Homes Are One of the Best Values in North Carolina Real Estate — If You Know the Rules.

In NC's rural markets, manufactured homes represent a real path to ownership that a stick-built home at double the price can't match. But the financing is different. The title process is different. And if you walk in without knowing what you're dealing with, you'll hit walls fast.

This guide covers everything NC buyers need to know: how homes are classified, which loan programs are available, what the HUD label requirement means, foundation certification, and how to make sure the deal you write can actually close the way you structured it.

Manufactured homes sit on rural lots, wooded tracts, and private acreage all across this state. Priced right, bought right — they're a serious asset. Priced wrong, bought without the right framework — they're an expensive lesson. Ninja Realty has worked these transactions. Here's the straight story.

Classification Matters

Real Property vs. Personal Property — This Single Factor Determines Your Financing.

Before you can even think about a loan, you need to know how the home is classified. This is the most important thing in any manufactured home transaction.

Real Property: The home is permanently affixed to land the owner also owns. The wheels, axle, and hitch have been removed. The home sits on a permanent foundation. The title has been surrendered and converted into the real property deed — meaning the home and land are treated as one piece of real estate. This classification opens the door to conventional, FHA, VA, and USDA financing.

Personal Property (Chattel): The home is on a rented lot, sits on land owned by someone else, or the title has never been surrendered. This is treated like financing a vehicle, not a house. Rates are higher, terms are shorter, and loan programs are limited.

Homes built before June 15, 1976 are classified as mobile homes — not manufactured homes — and do not meet HUD standards. Financing these through conventional, FHA, VA, or USDA is not possible. Cash or specialized portfolio lenders are typically the only options on pre-HUD homes.

Loan Programs

Five Ways to Finance a Manufactured Home in NC

Real property classification is required for government-backed programs.

FHA Loan

3.5% down with 580+ credit score. Home must be real property on a permanent foundation. Engineer certification required. Strong option for first-time buyers across NC.

VA Loan

$0 down for eligible veterans. Real property, permanent foundation required. VA appraisers are strict on condition. Best terms available when you qualify.

USDA Rural Development

$0 down in eligible rural NC counties. Income limits apply. Real property on permanent foundation required. If a current USDA loan is on the property, expect payoff statement delays — plan ahead.

Conventional (Fannie / Freddie)

Fannie's MH Advantage and Freddie's CHOICEHome programs cover manufactured homes meeting specific build and site standards. Higher credit scores typically required.

Land-Home Package

Combines new manufactured home + land purchase in one loan. Title surrender happens during the process. Lenders like 21st Mortgage and Triad Financial specialize here.

Required Documentation

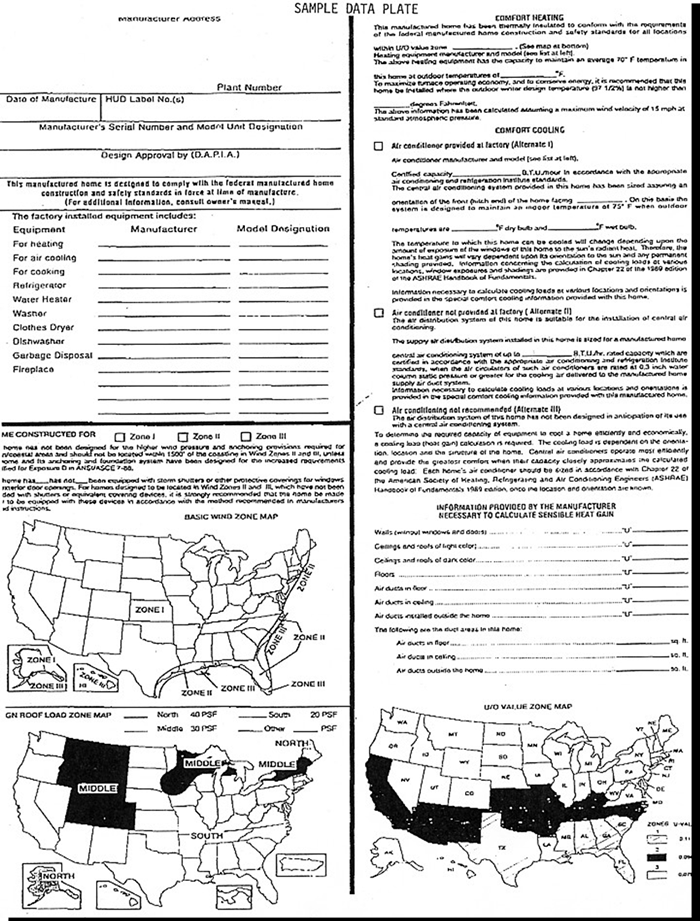

The HUD Tag & The Data Plate. Two Different Things — Both Matter.

Most people hear "HUD label" and think there's one thing to look for. There are actually two — and they serve different purposes. Both are required. Both matter to lenders. Here's the difference.

The HUD Certification Label (The "Tag")

This is the one most people mean when they say "HUD label." It's a small 2" × 4" red metal plate permanently riveted to the exterior of each section of the home — typically at the lower rear end. It cannot be easily removed without defacing it. Each tag has a unique number: three letters identifying the inspection agency, followed by a six-digit number.

The tag is the lender's visual confirmation that the home was built to federal HUD Construction and Safety Standards. One tag per section — so a double-wide has two. A triple-wide has three. If a tag is missing, lenders require a Letter of Label Verification from IBTS, HUD's record-keeping contractor. This is not a deal-killer. Ninja Realty facilitates the IBTS verification process on your behalf — it's straightforward and we typically have it back within a week.

The Data Plate (Inside the Home)

The Data Plate is a standard 8½" × 11" paper label affixed inside the home — usually in a kitchen cabinet, near the main electrical panel, or in a bedroom closet. It contains the home's full specs: manufacturer name and address, serial number, model, date of manufacture, and a map showing the Wind Zone, Roof Load, and Snow Load the home was designed for.

The Data Plate lists the certification label numbers for every HUD tag on the home. If a HUD tag is missing from the exterior, the lender will look for those numbers here first before requiring an IBTS verification letter. It also contains a list of major factory-installed appliances and equipment.

Check for the Data Plate during any showing. If it's missing or damaged, a replacement certification can be ordered through IBTS — and Ninja Realty facilitates that for our clients. We handle the paperwork, walk you through the process, and typically have verification back within a week. It's one less thing you have to figure out.

Foundation Certification — Required for Government-Backed Loans.

Owning the land isn't enough to qualify for real property financing. The foundation has to meet specific standards too. FHA, VA, and USDA all require compliance with HUD's Permanent Foundation Guide for Manufactured Housing (PFGMH). Key requirements:

- Permanent, frost-depth foundation — not pier blocks sitting on grade

- Wheels, axle, and tongue/hitch removed

- A licensed engineer certifies the foundation meets HUD guidelines

- Utilities permanently connected

- Permanent skirting — typically masonry or concrete block

If a home is already on the ground but hasn't been formally certified, a licensed engineer needs to inspect and certify it during the purchase process. Ninja Realty has engineers on hand who do this regularly and turn it around fast — no hunting for someone who's never touched a manufactured home before. It's a standard part of how we work these deals.

Own the Land. That's the Goal.

When you own the land your manufactured home sits on, you own the whole asset. No lot rent increases. No vulnerability if a park gets sold or redeveloped. And most importantly — your financing options expand dramatically. Real property classification requires land ownership, and real property financing is where the best loan terms live.

In North Carolina, there's no shortage of rural tracts where a manufactured home on owned acreage makes strong financial sense. You can often land a solid home, lot, well, and septic for a total cost that wouldn't cover a down payment on a major metro property. That's the opportunity — and it's the kind of deal Ninja Realty finds for buyers across NC every day.

Before You Write an Offer

The Manufactured Home Buyer's Checklist

-

✓

HUD labels present on all sectionsExterior metal plates, one per section — check visually before the offer

-

✓

Home built after June 15, 1976Pre-HUD "mobile homes" cannot be financed through FHA/VA/USDA

-

✓

Title surrendered — recorded as real propertyVerify with NC DMV or county register of deeds

-

✓

Permanent foundation installedMust meet HUD PFGMH standards for FHA, VA, USDA

-

✓

Wheels, axle and hitch removedRequired for real property classification

-

✓

Engineer foundation certification obtainedLicensed engineer must certify compliance with HUD guidelines

-

✓

Land in buyer's name (or concurrent with purchase)Land ownership is required for real property financing

-

✓

Manufactured home comps pulled for that countyAppraisers must use MH comps — not stick-built. Know the numbers before you offer

-

✓

Closing attorney experienced in MH transactionsNot every real estate attorney handles these regularly — ask before you contract

Common Questions

Questions Buyers Ask

Can I get an FHA loan on a manufactured home in NC?

Yes — if the home is real property, on a permanent foundation, has HUD labels, and the foundation has been engineer-certified to HUD PFGMH standards. FHA requires 3.5% down with a 580+ credit score. Ninja Realty works these transactions regularly. When all the pieces are in place, FHA is a solid path for NC buyers.

What happens if the HUD labels are missing?

Not a deal-killer. Lenders require a Letter of Label Verification from IBTS — HUD's official record-keeping contractor. Ninja Realty facilitates the entire process for you. We handle the paperwork and walk you through it, and verification typically comes back within a week. We find out during the showing, not at the closing table, because we check every time.

Can USDA be used on a manufactured home in NC?

Yes, in eligible rural counties. $0 down, income limits apply, real property with permanent foundation required. If the property already has an existing USDA loan, be prepared for payoff statement delays. USDA's Rural Development office can run slow — congressional escalation is often the most effective remedy if things stall.

How does the appraisal work on a manufactured home?

Appraisers must use comparable manufactured home sales — not stick-built homes — as comparables. In thinly-traded rural NC markets, comps can be limited. Ninja Realty pulls MH-specific comps for that county before any offer goes in, so you know the number your deal actually needs to appraise at before you're under contract.

Who should I call at Ninja Realty about a manufactured home?

James Hutson, Broker-in-Charge. We've worked manufactured home transactions across North Carolina — residential, land, and rural market deals. Call (252) 915-2311 or visit ninjarealtync.com.

Ninja Realty Knows This Market.

We check HUD tags, pull manufactured home comps, facilitate IBTS verification, and have engineers on hand for fast foundation certification.

Call us before you write the offer — not after something goes sideways.